April 1, 2026

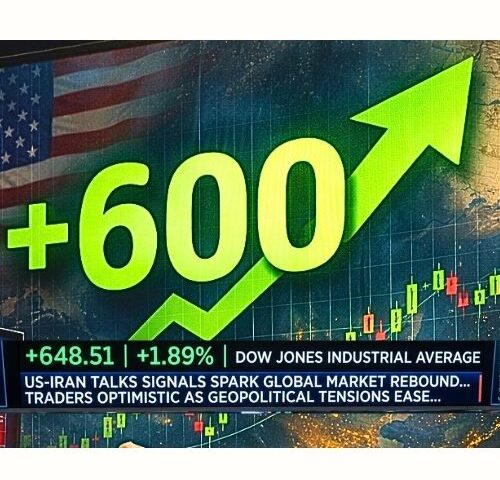

Global financial markets are navigating a high-stakes transition, as a mix of geopolitical signals, rising bond yields, and a deepening technology sector selloff reshape investor sentiment worldwide. After a sharp correction earlier this week, markets are now attempting a fragile rebound, driven largely by expectations that tensions around the Iran conflict may ease.

However, beneath the surface, structural risks remain firmly in place suggesting that this is not a simple recovery, but a broader recalibration of global market dynamics.

Geopolitical Signals Drive Short-Term Optimism

Investor sentiment received a temporary boost after Donald Trump indicated that the United States could exit the Iran conflict within weeks. The announcement, along with an upcoming national address, has fueled speculation that geopolitical tensions may de-escalate sooner than expected.

Markets responded quickly. U.S. futures ticked higher, while European and Asian equities showed signs of recovery. Oil prices, which had surged during the conflict, retreated below key levels as traders priced in a potential reduction in supply disruptions.

This reaction highlights a consistent pattern in global markets: even the possibility of geopolitical stability can trigger rapid inflows into risk assets.

Yet, this optimism remains highly conditional. Analysts caution that policy unpredictability continues to act as a major overhang, particularly given the shifting tone of U.S. foreign policy and its broader implications for global trade and alliances.

Tech Sector Remains Under Pressure

While geopolitical relief has supported broader indices, the technology sector continues to face significant headwinds. The recent selloff has been both sharp and widespread, signaling a deeper shift in how investors value high-growth companies.

The Nasdaq Composite has entered correction territory, falling more than 10% from its recent highs. This decline reflects a growing reassessment of valuations, particularly among companies that have benefited from artificial intelligence-driven enthusiasm over the past year.

Several major firms have led the downturn. Shares of Meta Platforms dropped sharply following a landmark legal verdict linking social media platforms to user addiction. The ruling has raised concerns about potential regulatory changes that could impact business models built on user engagement and digital advertising.

Similarly, Alphabet Inc. saw its stock decline as the implications of the verdict extended across the broader digital ecosystem.

The selloff has not been limited to these companies. NVIDIA Corporation and Amazon also posted notable losses, reinforcing the view that this is a sector-wide correction rather than isolated weakness.

For investors, this marks a critical shift—from growth optimism to risk reassessment.

Rising Bond Yields Tighten Financial Conditions

At the same time, macroeconomic pressures are intensifying. The surge in the 10-year U.S. Treasury yield to 4.43% is adding a new layer of complexity to the market environment.

Higher bond yields directly impact borrowing costs across the economy. Mortgage rates, business loans, and consumer credit are all becoming more expensive, which in turn can slow economic activity.

More importantly for equity markets, rising yields reduce the relative attractiveness of stocks—especially those that rely heavily on future earnings projections. Growth-oriented companies, particularly in the tech sector, tend to be the most sensitive to these shifts.

The result is a tightening liquidity environment, where capital becomes more selective and risk tolerance declines.

Corporate Developments Reflect Structural Shifts

Recent corporate announcements further underscore the changing landscape. Oracle Corporation revealed plans to cut thousands of jobs as part of a broader strategy to redirect resources toward artificial intelligence investments. The move reflects a growing trend among large tech firms to prioritize AI infrastructure while streamlining legacy operations.

Meanwhile, Microsoft is facing increased scrutiny after reporting one of its weakest quarters in years, raising questions about its competitive positioning in the rapidly evolving AI space.

On the global stage, competition is intensifying. Chinese AI firm Zhipu reported a significant surge in revenue, highlighting the accelerating race for dominance in artificial intelligence.

These developments point to a broader transformation within the tech sector—one that goes beyond short-term market fluctuations and into long-term strategic realignment.

Energy and Defense Markets React to Policy Signals

Energy markets have also experienced sharp volatility. Oil prices dropped significantly after signals that the U.S. could scale back its involvement in the Iran conflict. This decline reflects how quickly geopolitical developments can shift supply expectations and market sentiment.

At the same time, the defense sector remains in focus, as ongoing tensions continue to influence government spending priorities. Investors are increasingly looking at defense and energy stocks as potential hedges against geopolitical uncertainty.

Financial institutions such as Morgan Stanley have pointed to dividend-paying energy companies as potential beneficiaries in this environment, as investors seek stability and consistent returns.

Emerging Markets Show Mixed Signals

While global markets remain volatile, certain regions are showing resilience. In India, shares of IndiGo surged after the announcement of a new CEO, signaling confidence in leadership and growth prospects.

Across Asia, markets have responded positively to signs of potential de-escalation in geopolitical tensions. South Korea and Japan, in particular, have seen improved sentiment, although analysts warn that this optimism may be short-lived if underlying risks persist.

These mixed signals highlight the uneven nature of the current recovery, where localized gains coexist with broader global uncertainty.

A Market in Transition

Taken together, recent developments suggest that global markets are entering a transitional phase. The combination of geopolitical shifts, regulatory pressures, and tightening financial conditions is forcing investors to rethink traditional strategies.

Capital is increasingly moving away from high-growth, high-risk assets and toward more defensive sectors and fixed-income investments. At the same time, legal and regulatory risks are becoming a more prominent factor in valuation models—especially for companies operating in highly scrutinized industries.

This shift represents a move toward a more disciplined investment environment, where profitability, resilience, and risk management take precedence over rapid expansion.

Outlook: Volatility Likely to Persist

Looking ahead, markets are expected to remain highly sensitive to incoming data and policy signals. Key factors to watch include central bank communication, inflation trends, and further developments in the Iran conflict.

While the possibility of geopolitical relief offers a pathway to stabilization, the broader macroeconomic environment suggests that volatility is far from over.

For investors and businesses alike, the coming weeks will be critical. The decisions made during this period—whether to reduce risk, rotate assets, or double down on long-term opportunities—will shape performance in the months ahead.

The current market environment is defined by complexity and rapid change. What appears on the surface as a rebound is, in reality, part of a deeper structural reset.

Global markets are shifting away from an era of easy liquidity and aggressive growth toward one defined by tighter financial conditions, increased regulation, and heightened geopolitical awareness.

For those navigating this landscape, the message is clear: adaptability, discipline, and strategic foresight are no longer optional they are essential.

Stay ahead of global market shifts, tech trends, and geopolitical insights—explore more in-depth analysis at Daily Finance.