Oil’s war risk premium is unwinding fast after a two week truce and Strait of Hormuz reopening pledge, lifting stocks and Fed rate cut hopes even as geopolitical fault lines remain exposed.

Global markets are staging a powerful relief rally after Washington and Tehran agreed to a fragile two week ceasefire that reopens the Strait of Hormuz and temporarily averts a deeper Gulf energy shock. President Donald Trump paused planned strikes on Iranian infrastructure on Tuesday night in exchange for Tehran’s promise to allow safe navigation through the world’s most critical oil chokepoint.

The deal, brokered with last minute help from Pakistan and announced just before Trump’s deadline expired, instantly knocked crude prices back below the psychologically important 100 dollar mark and triggered a sharp risk on rotation across global assets. But with both sides treating the agreement as leverage rather than peace, investors are treating the move as a tradable truce, not the end of the crisis.

Oil’s war premium evaporates for now

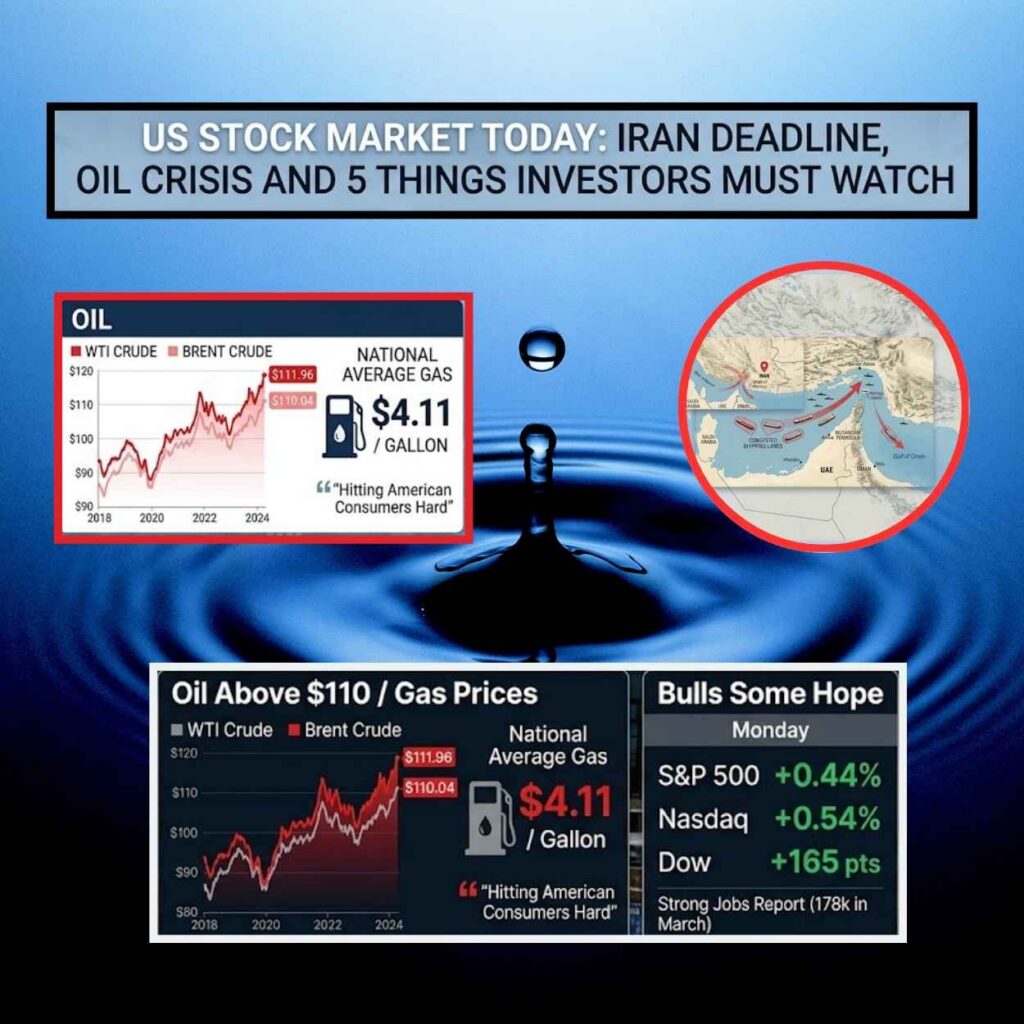

West Texas Intermediate (WTI) crude futures for May delivery tumbled roughly 15% on the headline, settling around 95.63 dollars per barrel by late Tuesday in New York trading. Brent crude slid in tandem, with some estimates putting the combined intraday move above 15–17%, one of the largest single session percentage drops since the Gulf War era.

The mechanics are straightforward. For six weeks, oil had been pricing in the risk that Hormuz, which carries a big share of global seaborne crude, could be partially or fully choked off by missile strikes, mines, or harassment of tankers. That war risk premium propelled Brent toward 120–130 dollars and pushed pump prices higher worldwide. By explicitly tying the ceasefire to immediate and safe transit through the Strait, the US Iran deal removed the most extreme near term disruption scenario at least for the next 14 days.

Traders responded by aggressively unwinding long positions and volatility hedges. Both benchmarks are still well above the roughly 70 dollar pre war range, underscoring that the market is discounting a pause, not a full normalization in Gulf supplies. Any hint of attacks on tankers or infrastructure could quickly re inflate that premium.

Equities cheer, safe havens stay alert

The oil plunge lit a fire under global stocks. US equity futures jumped, with S&P 500 contracts up over 2.5% and Nasdaq 100 futures gaining more than 3% in early trade, pointing to a strong open and pushing the S&P closer to fresh record territory. Asian markets followed through: indexes across Tokyo, Seoul and Mumbai logged gains of 3–6% as traders rushed back into cyclicals, financials and rate sensitive tech names.

Europe joined the party as well, with major benchmarks climbing on the prospect of lower energy costs and reduced tail risk to global growth. Airlines, shipping and energy intensive industrials led the rebound after weeks of underperformance.

Yet the message from safe haven assets is more nuanced. Gold, which had spiked on war fears, remains elevated even after giving back some gains, while silver and other precious metals continue to attract demand from investors hedging against both geopolitical flare ups and policy missteps. Bitcoin and other digital assets are also holding up, reflecting ongoing appetite for alternative macro hedges.

Fed rate cut hopes get a second life

The biggest macro shift for a US audience sits in the rates market. Treasuries rallied as crude collapsed, with two year yields dropping around 7 basis points and the 10 year sliding roughly 4 basis points in early Wednesday Asia trading. That bull steepening reflects a rapid rethink of the Federal Reserve’s reaction function now that the worst case oil price spike appears less likely at least temporarily.

Before the ceasefire, the Iran war had narrowed the Fed’s already tight path to easing. Sticky core inflation, strong US labor data and 100 plus dollar oil had prompted some Wall Street houses to scrap 2026 rate cut calls entirely and even float the risk of renewed hikes. The March FOMC dot plot penciled in just one 25 basis point cut this year off a 3.50–3.75 percent policy range.

Post ceasefire, rate futures and overnight index swaps are again leaning toward a softer stance. Traders now see materially higher odds around 60% in some estimates of at least one cut by December, and some desks are tentatively reopening scenarios with two small moves if oil drifts lower and headline inflation rolls over.

For US equity investors, that combination of lower energy prices and revived Fed cut hopes is potent. It eases stagflation fears, supports valuations in growth and tech, and offers relief to credit sensitive pockets like high yield and leveraged loans that had started to wobble under higher for longer assumptions.

Gulf risk hasn’t gone away

Despite the strong market response, the ceasefire itself is narrow, time bound and fragile. Trump has framed the deal as leverage to secure a broader settlement, while Iranian officials stress that safe passage through Hormuz will be managed by their military and subject to technical limitations, leaving room for friction.

Diplomats are scrambling to turn the two week window into a more durable framework, with talks expected in Islamabad and other regional capitals. But the underlying flashpoints Iran’s nuclear program, proxy networks, Israel’s security, and US sanctions remain unresolved.

For global investors, that means positioning for volatility rather than a straight line normalization. Energy importers from Europe to Asia gain breathing room from sub 100 dollar crude, but supply chains, shipping insurance and Gulf risk premia will continue to whipsaw with every headline out of the Strait of Hormuz.

If the truce holds and is extended, the narrative could shift toward softer inflation, friendlier central banks and a more durable risk on regime. If it breaks, markets will quickly reprice a return to triple digit oil, a tougher Fed, and renewed pressure on global growth. For now, the message from the Gulf is simple: enjoy the rally, but keep one eye on Hormuz.