US Stock Market Today Slips as War Fears Drive Inflation Higher and Erase Rate Cut Hopes

Stagflation signals are mounting. With the US Composite PMI at an 11-month low and input costs surging at their fastest pace in nearly a year, the Federal Reserve finds itself boxed in — and markets are repricing every assumption built on 2025’s rate-cut narrative.

Geopolitical risk has moved from background noise to front-and-center market driver — and it is landing on an economy that has limited capacity to absorb the hit.

The latest Flash PMI data from S&P Global delivered a double verdict on Thursday: US business activity contracted to an 11-month low of 51.4 in March, while input costs accelerated at their fastest pace in nearly a year. The culprit, in both cases, is the same — energy prices spiking on the back of sustained Middle East conflict, with no clear resolution in sight.

What made Thursday’s data particularly uncomfortable for investors was the combination. Slowing growth alongside rising prices is not just a drag — it is the specific configuration that limits the Federal Reserve’s options most severely.

The Fed’s Hands Are Tied

Nothing illustrates the Fed policy bind more sharply than the collapse in rate-cut expectations. According to CME Group’s FedWatch Tool, the probability of a Federal Reserve rate cut in 2026 has fallen from 95% just one month ago to 8% today. That is not a gradual shift — it is a repricing event.

More telling: markets are now assigning a 16% probability to a rate hike in 2026, a scenario that was virtually unthinkable as recently as late February. The math is straightforward. If inflation 2026 re-accelerates faster than growth recovers, the Fed cannot cut. And if cost pressures persist long enough, the next move may be up, not down.

“The rate-cut trade that anchored 2025’s equity rally is being systematically unwound. What replaces it is still unclear — and that uncertainty is the trade right now.”

Markets Desk Analysis · March 26, 2026Fed Chair messaging will be scrutinized closely in the weeks ahead. Any shift toward a more hawkish tone — particularly referencing energy-driven inflation as persistent rather than transitory — could accelerate the repricing further.

Gold Prices Jump as Safe Havens Surge

Gold prices surged nearly 4% in early Thursday trading, benefiting from a weaker US dollar, softening Treasury yields, and a classic flight-to-safety dynamic that tends to accelerate when geopolitical risk feels open-ended. The move puts gold firmly back in institutional portfolio conversations that had largely shifted to equities during last year’s rally.

The combination of a falling dollar and rising gold prices sends a clear message: global investors are hedging against a scenario where US monetary policy stays constrained longer than expected, and where real yields compress further if growth disappoints.

Stock Market Today: Divergence, Not Direction

Today’s US stock market is not moving as a unified trade — it is splitting along structural fault lines. Companies with secular growth tailwinds are holding or advancing. Companies exposed to rate sensitivity and consumer discretionary pressure are giving ground.

Arm Holdings (+13%) was the session’s standout performer, rallying sharply after reaffirming guidance and raising its operating margin targets. AI-driven semiconductor demand continues to act as a buffer against macro headwinds, and Arm’s results confirm the structural demand story remains intact regardless of PMI prints.

Chewy (+7%) beat expectations on both revenue and earnings, with management issuing a positive forward outlook. Essential consumer spending — particularly pet care — is demonstrating the kind of demand inelasticity that makes it a defensible position in a slowing economy.

KB Home (−1.8%) missed on both top and bottom lines, underscoring the compounding pressure on homebuilders: elevated mortgage rates reducing buyer qualification, rising material costs squeezing margins, and demand uncertainty capping pricing power. Housing remains one of the most rate-sensitive sectors in the market, and the new rate outlook is not friendly to it.

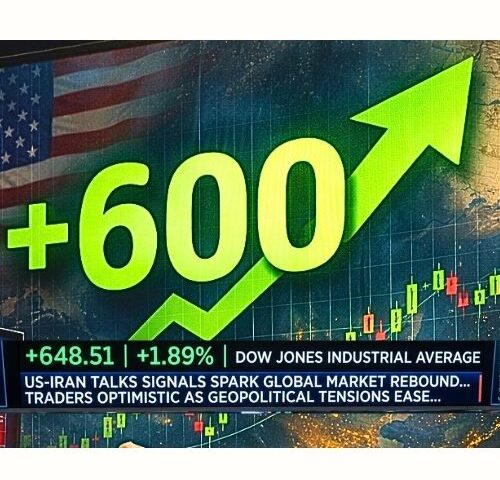

Dow Holds, But the Margin Is Thin

The Dow Jones Industrial Average closed 0.65% higher on Wednesday, supported by cautious optimism around potential diplomatic progress in the Middle East. But futures are pointing lower into Thursday’s open, and the session’s gain has the feel of relief rather than conviction.

The underlying picture remains fragile. Volume patterns suggest institutional positioning is defensive, not constructive. Until there is either a geopolitical de-escalation or a clear signal from the Fed on its tolerance for inflation persistence, the path of least resistance for equities is sideways to lower.

Strategic Positioning in a Stagflation-Risk Environment

The trades working in this environment share a common characteristic: insulation from both rate risk and growth deceleration. AI infrastructure, essential services, and real assets like gold are performing. Rate-sensitive sectors — housing, long-duration growth, consumer discretionary — are under pressure.

The next two to three weeks are pivotal. Any escalation in Middle East tensions that pushes energy prices materially higher will force a further repricing of the inflation 2026 outlook. Conversely, credible de-escalation could restore some of the rate-cut probability and with it, significant equity upside in the sectors that have sold off most sharply.

Until then, the market’s message is unambiguous: geopolitical risk is now a macro variable, and portfolios that have not accounted for it are running an unhedged position.